I finally summoned the motivation to read through a month's worth of AT&T/T-Mobile merger filings. Did I learn anything new? No, not really. I've been following AT&T/T-Mobile happenings closely on Twitter and in the news, and I've been waiting for a big story to break that I can write about without sounding like I'm just reiterating what everyone else has been saying. Ironically, the latest big story is literally about merger supporters reiterating what AT&T has told them regarding the alleged benefits of the merger. Last week, the president of GLAAD resigned after it was discovered that the organization submitted a letter in support of the merger which AT&T had written for them. I don't have a problem when numerous companies/organizations submit essentially the same comments in proceedings, but rubber-stamping form letters that supposedly express a group's unique perspective is just deplorable public policy—especially if the letters are written by a company that gives the organization money. GLAAD is not the only organization with questionable motives in support of AT&T/T-Mobile, and this situation has made me extremely suspicious of all of the filings in support of the merger submitted by groups who basically have no clue about the potential harms the merger will cause. No offence to the myriad groups of hotel owners, minority businessmen and women, cattle ranchers, pipefitters, local tourism boards, women farmers, chambers of commerce, Spanish language journalists, Asian-Pacific Islanders in America, senior citizens, aerospace mechanics, Lupus foundations…and the International Rice Festival?!? It's not that I don't value your opinions—I just don't think they are your opinions. But, I believe that you believe that the AT&T/T-Mobile merger will benefit your constituents even though I don't see any evidence to back these positions.

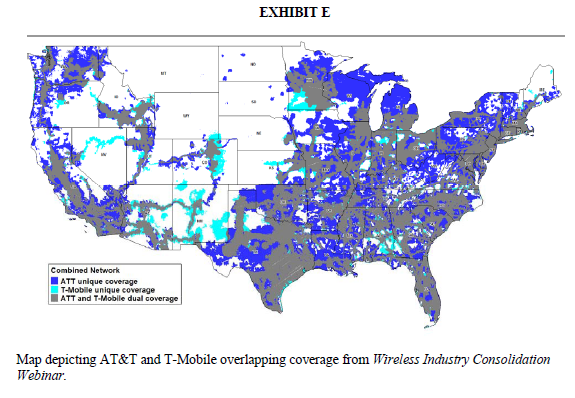

Sarcasm aside, I was really concerned about the number of rural organizations that voiced support for the merger, especially because rural telecommunications providers are largely opposed to the merger. The Rural Telecommunications Group (RTG), a leading organization of rural wireless providers and a sponsor of the No Takeover Project, noted in their May 31 petition to deny that "it is rural consumers who stand to lose the most in a post-merger marketplace," and "the unimpressive truth is that the addition of T-Mobile's network to AT&T's existing footprint only increases the geographic size of AT&T's network by a mere one percent" (pg. 14). Unfortunately, rural consumers, governments and organizations have apparently been duped by *someone* into thinking that AT&T will become some kind of wizard or genie who will magically make low-cost and high-quality broadband appear in areas with 2 customers per square mile. The West Virginia Farm Bureau argues that "As West Virginians fight lingering unemployment and dig deeper into their pocketbooks for gas and commodities, most of us would welcome new opportunity—and lower prices. That trend may be just over the horizon, thanks to the pending merger between AT&T and T-Mobile" (pg. 1). The WVFB also details how important broadband is to farmers and rural residents because it enables them to "track markets, research equipment and methods, and communicate with markets around the world…develop and expand their farms with web-based sales…sell directly to markets and individual customers around the world." WVFB, I couldn't agree more, but I think this comment would be more appropriate in the USF Reform proceeding. West Virginia is notoriously one of the worst states for wireless service, and I don't see how AT&T-Mobile will suddenly decide that WV is an attractive market with a high ROI. I sincerely hope the WV farmers get the high-speed broadband that they deserve, but I just don't think the AT&T/T-Mobile merger will do anything to achieve this goal. Here's an easy test you can utilize to get an idea of whether or not AT&T/T-Mobile will serve your rural area post-merger:

- Is there currently good-quality AT&T service in your rural area?

- Is there currently good-quality T-Mobile service in your rural area?

- Bonus question—is there a good-quality small/regional wireless carrier in your rural area?

The rural organizations who support the merger predictably and erroneously claim that the merger will create all these wonderful opportunities for their respective groups. The Montana Farmer's Union argues that "the combined resources of AT&T and T-Mobile, along with an additional $8 billion investment in infrastructure, will make mobile broadband accessible to almost the entire country's population." The Arizona Cattle Feeder's Association expects the merger will help improve border security, for apparently they have "endured no greater challenge to [their] business and quality of life than border security." The Women Involved in Farm Economics believe that the merger should be approved because "better wireless service has the potential to improve non-farm economic life in many hard-hit rural areas that have seen tragic declines in manufacturing and building jobs," and "for an increasing number of farmers and ranchers, advanced wireless systems hold remarkable promise for better, more productive lives." It really hurts me to argue against rural organizations who are clearly in need of reliable wireless broadband and who understand the importance of broadband for rural areas, but I feel strongly that these groups are wrong to assume that the AT&T/T-Mobile merger will make a difference in their rural lives. If they put half as much effort into advocating for RLECs in the USF Reform proceeding, I would probably be able to sleep better.

As evidenced by RTG's exceptional arguments against the merger, rural telecommunications carriers have vastly different opinions than rural consumers/organizations. Actually, it isn't fair to include consumers in the groups of supporters of the merger—AT&T isn't paying off individual consumers (yet anyway, as far as I know), and one consumer comment that likened AT&T to a rapist has been haunting me for the last month. I've seen very little evidence that end-use consumers support the merger, rural or otherwise. Anyway, I was pleased to see that several Iowa rural telecommunications providers submitted opposition comments. FMTC Wireless, Breda Telephone Corporation, Webster-Calhoun Cooperative Telephone Association, and Marne & Elk Horn Telephone Company, all RLECs and providers of iWireless service, voiced their concerns about the merger's potential impact on their "continued ability to provide high-quality advanced wireless telecommunications services to communities and underserved areas in rural Iowa." Each of these companies echoes the concerns raised by iWireless, and they argue that "the iWireless partnership with T-Mobile has been extremely important to our businesses. It has given us access to partitioned spectrum in our rural communities and it has helped to create a larger market and more diverse ecosystem for GSM and UMTS/HSPA infrastructure, equipment and handsets. It has also given us a reliable partner for inbound and outbound roaming and it has given our customers access to a ubiquitous nationwide GSM/UMTS network with voice and high-speed data capabilities."

If the merger is approved, iWireless faces a precarious situation. Although iWireless does not specifically ask for the merger to be rejected, they do ask for the FCC to "agree to certain commitments to foster the continued prevision and expansion of wireless services in rural areas" (petition to deny filing, pg. i.). iWireless is a close relative to T-Mobile (here's how they explain the relationship: "Deutsche Telekom holds a 100 percent ownership interest in T-Mobile, which in turn indirectly holds a 100 percent ownership interest in VoiceStream PCS. VoiceStream PCS holds a 54 percent interest in Iowa Wireless, and DT is authorized by the Commission to hold up to a 60 percent indirect interest in Iowa Wireless, pg. i.). Not to make things more confusing, but then iWireless is in "contractual relationships with 76 small independent telephone companies to extend the reach of its network to include remote rural areas." From what I've been told, the iWireless partnership has been very beneficial for Iowa RLECs and rural customers, and it has facilitated considerable investment in rural wireless networks.

As a subsidiary of T-Mobile, iWireless faces an uncertain or at least challenging road ahead. AT&T has remained mum on the subject of the fate of iWireless if the merger is approved, and "since the announcement of the AT&T/T-Mobile transaction, Iowa Wireless has not been able to obtain any information regarding how—if at all—AT&T will incorporate Iowa Wireless into its long-term plans, nor has Iowa Wireless been able to determine what impact, if any, the transaction will have on Iowa Wireless's rural customers with respect to continued network access at reasonable rates" (pg. 4).To me, this sounds very bad—for RLEC partners and rural consumers especially. To me, this is evidence that AT&T does not have a strong commitment to rural areas, despite what they may claim or convince/pay niche rural groups to claim for them. iWireless has 250 stores and authorized dealers in the Midwest, which surely employ thousands of people. iWireless also provides service to rural areas that "do not have the necessary subscriber densities or potential returns on investment to attract large carriers to invest in the infrastructure…required to serve residents in those locations" (pg. 3). iWireless stops short of outright opposing the merger, but they do request that the FCC impose a variety of conditions such as ensuring that AT&T continue to provide roaming for iWireless partners and making sure that AT&T does not repurpose iWireless spectrum.

I personally do not like the division that has emerged between rural telecommunications carriers and rural consumer/trade organizations, but misinformation is clearly to blame. I encourage RLECs who oppose the merger to come up with creative ideas to educate and inform your consumers about the likely outcome of the merger—that rural areas will not benefit, competition will decrease, jobs will be lost, prices will increase, quality will be compromised, etc. There is plenty of evidence to illustrate the multitude of harms that could befall rural consumers, and there are many advocacy groups who are working tirelessly to provide great information about the merger—information not written by one of the parties involved in the merger!

I will be watching for new information about the future of iWireless, and I am hoping someone will tell me why exactly the International Rice Festival supports the merger.

Next week I hope to look at some international examples of successful USF models. A kind reader from Pakistan e-mailed me some information today about Pakistan's USF program, and I am excited to learn about it.

Cassandra Heyne

ruraltelecommentary@gmail.com